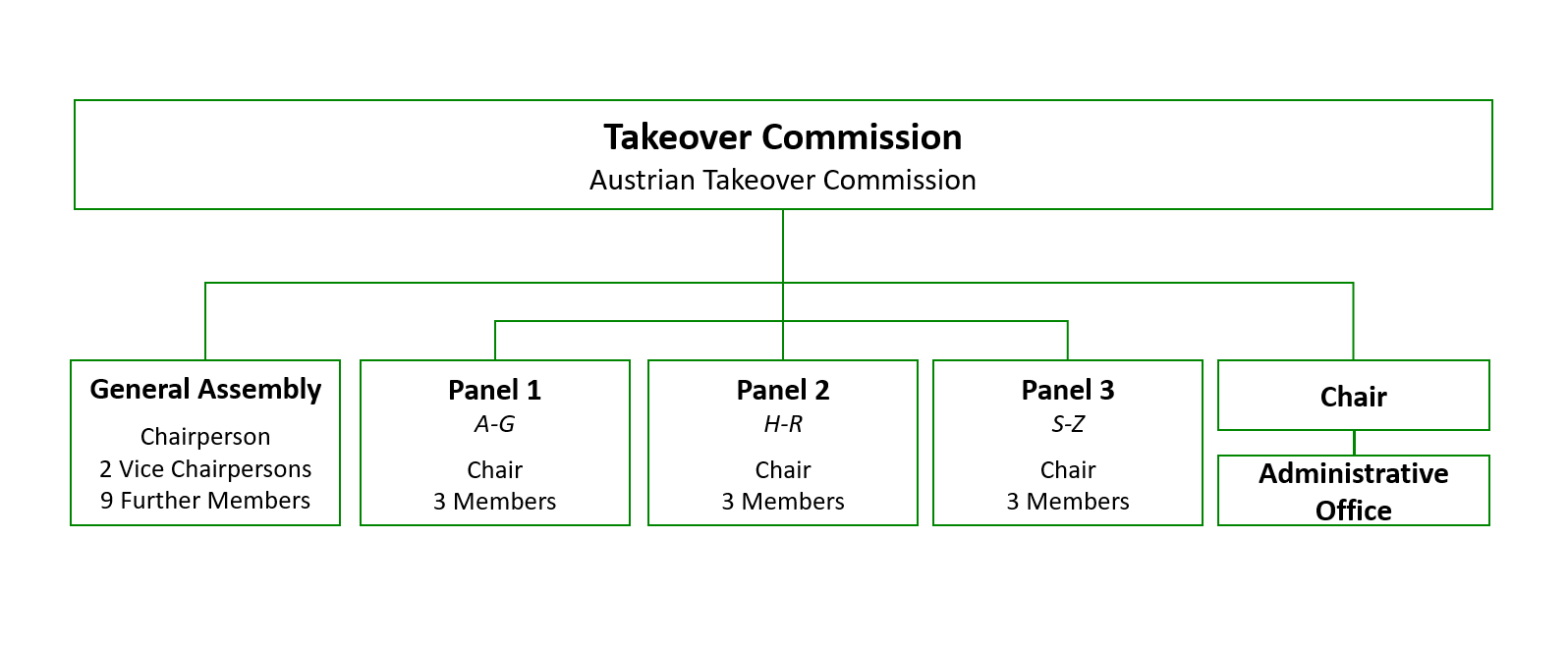

The Takeover Commission is an independent authority established within the organisational framework of Wiener Börse AG, the exchange operating company of the Vienna Stock Exchange. The Takeover Commission consists of twelve part-time members and an administrative office. Its primary responsibility is to monitor the entire bidding process and to assess whether or not a mandatory bid is required.

Tasks

When public bids are made to buy securities of listed companies, there is not only a need to protect minority shareholders, but also to follow an orderly procedure in the interest of both the offeree company and the capital market. First, there is a risk that biased information and an unregulated procedure would render it impossible for the holders of free-floating shares to reach informed decisions on whether or not to accept such a bid. Second, minority shareholders run the risk of their shares losing value as a result of a new strategy being pursued after control of a company has been taken over. It was especially with this set of problems in mind that the Takeover Act was adopted to provide a regulatory framework and to mitigate risk.

- The primary, the purpose is to create a minimum level of regulation for public takeover bids.

The Takeover Act stipulates, for instance, the information that must be included in the offer documents and the minimum offer period. The Takeover Act also defines measures to prevent potential insiders from taking advantage of inside information. The management of the offeree company (= the company whose equities are to be bought) must generally behave in a neutral manner, must not frustrate the bid and must give the shareholders an assessment as to the reasonable nature of the bid.

- A second key topic regulated by the Takeover Act refers to mandatory bids:

Anyone who obtains a controlling interest in a listed company (e.g., by acquiring the majority holding from the previous majority shareholder) must also submit a bid to the other shareholders; i.e., no one should be forced to remain with the company under a new management. Thus, when there is a change in control, any existing shareholder may opt to sell shares (for cash). The law provides for exceptions to such mandatory bids, in particular, in cases in which control is taken over for the purpose of restructuring or in similar circumstances.

The Takeover Act is based on five principles, which not only clearly reflect the underlying intentions, but also have to be taken in consideration when applying the Act (cf. §3):

- Equal treatment of all shareholders of the offeree company

- Sufficient time and information for the addressees of public bids

- The officers and bodies of the offeree company must show neutral and objective conduct

- No distortions of the equity market in respect of the companies involved

- Speedy completion of the takeover procedure

The purpose of such measures is to make Austrian companies listed on the Vienna Stock Exchange more attractive to investors from Austria and from abroad and to ensure that the legal framework for the Austrian capital market is in line with the releavant best international practices as expected by private and institutional investors.

For more about the Austrian Takeover Act, please see

Legal Basis.